UCITS vs US ETFs: Which Is Better for Non-US Investors? (2026)

UCITS vs US ETFs: The Hidden Tax Traps Costing Southeast Asia Expats Thousands

Most expatriates in Southeast Asia are unknowingly holding the wrong investment vehicle. If you own US-domiciled ETFs, such as those trading on the NYSE or NASDAQ under tickers like SPY or QQQ, you are exposed to two tax drags that your broker almost certainly never mentioned: a 30% dividend withholding tax and a US estate tax liability that kicks in the moment your portfolio crosses $60,000. This post explains exactly what those risks mean for your wealth, and why UCITS-domiciled funds eliminate both.

Last updated: 23 April 2026

The 30% Dividend Withholding Tax Most Expats Are Already Paying

When a US-domiciled ETF pays out dividends, the IRS automatically withholds 30% of that distribution before it ever reaches your account. This applies to any non-US person holding US-sited assets, regardless of where you live or what passport you hold.

If you are a British engineer based in Kuala Lumpur holding $300,000 in a US S&P 500 ETF with a 1.5% dividend yield, that generates roughly $4,500 in annual dividends. The IRS takes $1,350 before you see a cent. Over ten years, compounded, that drag quietly erodes a significant portion of your returns.

Why Your Broker Doesn't Flag This

Most international brokers process this withholding automatically and report it as a line item on your annual statement. It does not appear as a fee. It does not appear as a charge. It looks like a tax you cannot control. Many investors assume it is unavoidable. It is not.

How UCITS Funds Handle Dividend Tax

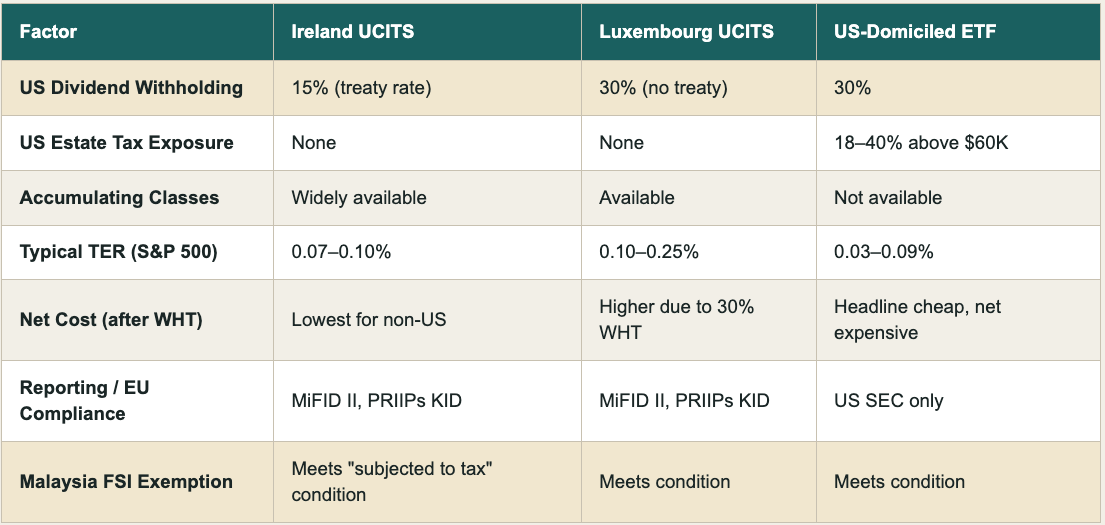

UCITS funds domiciled in Ireland, the most common jurisdiction for this structure, benefit from a US-Ireland tax treaty that reduces the withholding rate on US dividends to 15% at the fund level. Because the fund itself is the legal recipient of the dividends, that reduced rate applies automatically. You do not need to file anything. You do not need a treaty claim. The structure does the work.

For accumulating share class UCITS funds, dividends are reinvested inside the fund rather than distributed. There is no dividend event at your level, so no withholding tax trigger. Your entire return compounds without that drag.

The $60,000 Estate Tax Trap Most Expats Have Never Heard Of

This is where it gets serious, and where most advisors fail their clients entirely.

The United States imposes estate tax on US-sited assets owned by non-US persons at death. The exemption threshold for non-resident aliens is $60,000. That is not a typo. US citizens benefit from an exemption above $12 million. You, as a non-US expat, get $60,000.

Above that threshold, the US estate tax rate begins at 18% and climbs to 40% on amounts over $1 million. If a German executive based in Singapore holds $500,000 in US-domiciled ETFs and passes away, his estate faces a US estate tax bill of up to $176,000 before his family receives anything. That money cannot be recovered. It is gone.

What Counts as a US-Sited Asset

Any ETF or fund incorporated in the United States is a US-sited asset for estate tax purposes. This includes SPY, QQQ, VTI, and the vast majority of ETFs promoted through international brokerage platforms. The fact that you live in Malaysia, Thailand, or Vietnam does not change the situs of the asset.

Why UCITS Funds Are Outside US Estate Tax Reach

A UCITS fund domiciled in Ireland or Luxembourg is not a US-sited asset. It is an Irish or Luxembourgish legal entity that happens to invest in US stocks. Your estate holds shares in that Irish fund, not directly in US equities. The US estate tax rules do not apply. Your beneficiaries inherit the full value.

This is not a loophole. It is the fundamental legal distinction between asset domicile and underlying investment exposure. You can track exactly the same index, hold exactly the same underlying stocks, and pay a similar or lower total cost, while eliminating US estate tax exposure entirely. As discussed in Think You're Diversified? Think Again: A Guide for High-Income Expats, the real risk in a portfolio is often not what you can see, but what the structure beneath it is quietly doing to your wealth.

How Do Ireland, Luxembourg, and US Fund Domiciles Compare?

Ireland is the default choice for most expats because it combines the lowest withholding rate with full estate tax protection. Luxembourg works too, but at a higher tax cost. US domicile is the worst structure for any non-US investor.

The bottom line: Irish-domiciled UCITS funds give you the same market exposure as US ETFs, at a lower net cost, with zero estate tax risk. Luxembourg UCITS work for estate tax protection but cost more due to the missing treaty. US-domiciled ETFs are the worst option for any non-US investor with assets above $60,000. For a deeper look at how this interacts with Malaysia's tax rules, see our guide on Malaysia's foreign-sourced income tax exemption.

Choosing the Right UCITS Fund: What Actually Matters

Not all UCITS funds are equal, and selecting the wrong one still costs you money. Here is what to evaluate.

Accumulating vs Distributing Share Classes

Accumulating share classes (often labelled "Acc") reinvest dividends internally. Distributing share classes ("Dist") pay them out. For most expats in Southeast Asia with no immediate income need from their portfolio, accumulating classes are more efficient. There is no dividend event, no withholding trigger, and the compounding is uninterrupted.

Total Expense Ratio and Tracking Error

The most popular Irish-domiciled UCITS equivalents of major US ETFs carry expense ratios between 0.05% and 0.20%. That is comparable to, and in many cases lower than, the US-domiciled equivalent once you account for the withholding tax drag on dividends. Tracking error, how closely the fund follows its benchmark, should also be assessed before committing capital.

Currency Denomination

UCITS funds are typically available in USD, GBP, EUR, and SGD share classes. If you earn in USD and plan to spend in GBP in retirement, choosing the correct currency denomination at the fund level matters. This is one of the reasons that how busy expats can turn currency swings into savings is worth reading alongside this post. Currency exposure inside your investment structure is a separate decision from the fund's underlying holdings.

Frequently Asked Questions

Q: What is the difference between a UCITS fund and a US-domiciled ETF? A: A UCITS fund is regulated under European Union law and typically domiciled in Ireland or Luxembourg. A US-domiciled ETF is incorporated in the United States. Both can track the same index, but the legal domicile determines your tax exposure. For non-US expats, UCITS funds eliminate US estate tax risk and reduce dividend withholding tax through treaty structures.

Q: How much dividend withholding tax do I pay on US ETFs as an expat? A: Non-US persons holding US-domiciled ETFs are subject to a 30% IRS withholding tax on dividend distributions. Irish-domiciled UCITS funds benefit from a US-Ireland tax treaty reducing this to 15% at the fund level. Accumulating UCITS share classes avoid a distribution event entirely, deferring any tax trigger until you sell.

Q: Does the US estate tax really apply to expats holding US ETFs? A: Yes. The US imposes estate tax on US-sited assets owned by non-resident aliens at death, with an exemption of only $60,000. Above that threshold, rates range from 18% to 40%. If you hold US-domiciled ETFs, those assets are US-sited regardless of your country of residence. UCITS funds domiciled in Ireland or Luxembourg fall outside this rule.

Q: Can I hold UCITS funds through a standard brokerage account in Southeast Asia? A: Many international brokers accessible from Malaysia, Singapore, Thailand, and Indonesia offer Irish-domiciled UCITS ETFs. However, availability varies by broker and by your country of tax residence. It is worth confirming that your brokerage reports correctly and that the fund structure is appropriate for your specific situation before investing.

Q: Are UCITS funds more expensive than US ETFs? A: Not materially. The expense ratios on major Irish-domiciled UCITS ETFs are typically between 0.05% and 0.20%, comparable to their US equivalents. When you factor in the 30% dividend withholding drag on US-domiciled funds, UCITS funds are often cheaper on a net return basis over a full investment cycle.

Q: Does switching from US ETFs to UCITS funds trigger a tax event? A: Selling your existing US-domiciled ETFs may trigger a capital gains event depending on your country of tax residence and the gain accrued. Tax rules vary by jurisdiction and this is not tax advice. You should review your specific situation with a qualified advisor before making any changes to your portfolio.

If you are holding US-domiciled ETFs and have never been told about dividend withholding tax or the $60,000 estate tax threshold, this is exactly the conversation you need to have. No pitch, no pressure, just clarity on where you stand and what your options are. Book a no-obligation call with Ciprian.

This content is for informational purposes only and does not constitute personalised financial, investment, or tax advice. By reading this post, you agree to our disclaimer.